Accordingly, home health has become at the forefront of many discussion within the healthcare industry. Health systems contemplate better ways to integrate home health services into their continuum of care offerings while home health operators are positioning themselves to financially benefit from increasing demand and interest in the space. Meanwhile, many health systems are exiting this business. In FYE 2016, there were approximately 55 announced home health transactions with an estimated value of $1.2 billion.1 Overall, there is a surge in market consolidation and / or strategic positioning in the home health space.

MARKETPLACE DYNAMICS

The home health services industry can be characterized as highly fragmented, where above-average growth potential is challenged by profit margin pressures. As broadly defined, the $88.8 billion home care industry is estimated to be growing 6.7% per annum2. With over 12,400 Medicare – certified home health agencies3, the top ten operators represent less than 21% of the market and the largest operator (Kindred Healthcare4) has a 5.8% market share5. The following chart is representative of the market’s fragmentation.

Since the rebasing of the Medicare payment system in 2010 as a result of the Patient Protection and Affordable Care Act, reimbursement for home health services have been negatively impacted.6 More recently, CMS’s final rule for 2017, after all policy changes, continued the downward reimbursement trend for home health services resulting in a net reduction of approximately 0.7%.7

Starting in 2017, CMS also updated its Conditions of Participation (CoP)8 to include additional communication, coordination and documentation requirements. These increased compliance standards are causing some operators to lose revenue opportunities if they do not make investments in information and communication technology. As a result of these changes, Medicare margins of freestanding home health service agencies have generally declined. Transaction decisions are now more critical as scale is becoming increasingly important to withstanding reimbursement and compliance headwinds.

TRANSACTION ENVIRONMENT

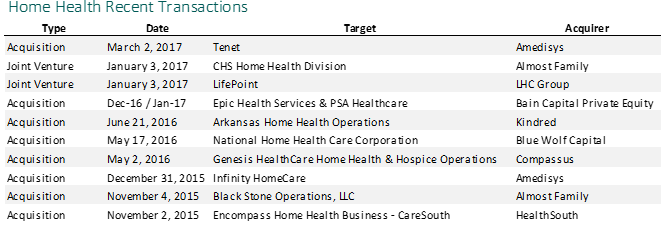

While transaction activity amongst independent operators has been more prevalent, recent announced deals and market participant commentary suggests health systems are becoming more engaged. Reasons for increased health system interest in the home health space vary from the ability to drive population health initiatives to removing (i.e. divesting) or improving (i.e. partnering) non-core businesses which may or may not be profitable inside the larger organization.

During 2016 two of the largest publicly traded home health operators in the nation, Almost Family (NASDAQ: AFAM) and LHC Group, Inc. (NASDAQ: LHCG), acquired home health and hospice operations by entering into partnerships with health systems. In October 2016, Almost Family announced a partnership with Community Health Systems (NYSE: CYH) by acquiring 80% of its home health business for $128 million. In a recent Almost Family investor presentation, management indicated joint ventures are increasingly becoming an important “go-to market” strategy in post-acute.9

LHC Group has a long history of strategic partnerships with health systems. In November 2016, LHC Group, Inc., announced it would partner with LifePoint Health (Nasdaq: LPNT) to jointly own and operate home health and hospice agencies. It now has 150 joint ventures under management and this strategy is expected to grow. LHC Group’s CEO Keith Meyers made the following comment on March 9, 2017, during the Q4 2016 earnings conference call:

“We continue to evaluate a robust pipeline of potential joint venture and freestanding transactions…we can operate very effectively in any market and as a result, are focused on hospital and health system joint venture expansion in all 50 states.”

While some health systems are engaging in partnership activities, others are outright selling their non-core home health business lines. Shortly after CHS announced its deal with Almost Family, Tenet Healthcare (NYSE: THC) announced it had entered into a letter of intent to sell home health and hospice businesses. Additionally, at a recent Barclays Global Healthcare Conference10, Benjamin Breier, CEO of Kindred Healthcare, Inc. stated the following:

“I think that referral sources are having to decide whether they want to be in that business or not. I mean, I think if you just look over the last 6 months, you’ve seen the — at least I think the 3 of the 4 largest for-profit hospital companies have also left all of their home health and hospice assets…they didn’t want to be in those businesses. You have others that, I think, see a lot of the same growth characteristics that we talked about and would like to get into it…I would say, over the last 6 months or more, it seemed like they’re getting out of it more than they are necessarily getting into it.”

Clearly, the outlook for home health transactions during FYE 2017 is strong. The observed industry fragmentation and growing importance of home health as a preferred patient destination will continue to create robust joint ventures, strategic partnerships, and acquisition opportunities.

In addition to the health system transactions, there continues to be a steady amount of other activity by specialized for-profit operators. Specialized operators are likely to be more aggressive in pursuing growth strategies to align with local health systems or execute upon market consolidation strategies. The specialized home health operators can manage staffing costs and quickly adapt to a more compliant-driven, lower reimbursement environment. As a result of their expertise, they may be purchasing, joint venturing or simply providing management services to the home health entities in the market.

STRATEGIC DECISION CONSIDERATIONS

As with any major decision in the healthcare industry, financial trends and regulatory considerations are critical. Whether the decision is to own/operate, JV, divest, or enter into a management agreement, there are important financial and regulatory considerations to each strategy.

From a financial perspective, understanding reimbursement, competition and current multiples are important first steps. Subsequently, conducting thorough due diligence on the operations and any proposed partner is time consuming, but crucial. At the same time, the regulatory framework of healthcare must always be integral to a transaction decision. Numerous regulations surround healthcare covering everything from licensure to the price paid in a transaction or compensation arrangement.

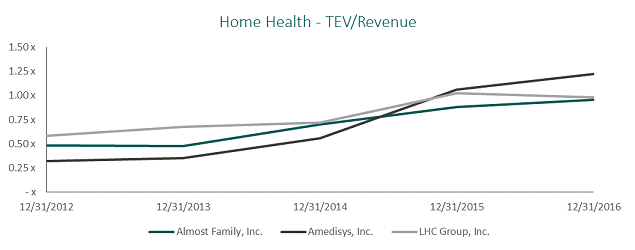

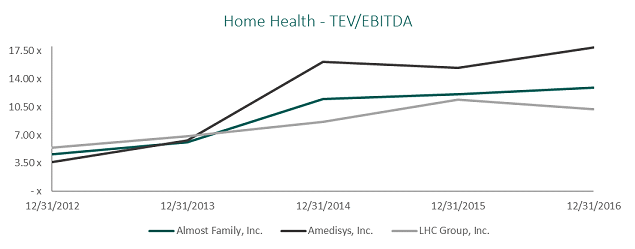

As it relates to the financial decision making process, one of the first metrics typically considered in the context of a transaction are current market multiples. The multiples for home health agencies continue to be strong, and trending upwards. Most industry participants analyze revenue and / or EBITDA multiples when evaluating potential acquisitions or joint ventures. The chart below references these multiples11 for the public home health companies. It should be noted that these organizations are large and diversified, therefore the implied trading multiples are often not applicable for single stand-alone agencies.

Numerous factors impact multiples of a business, and any buyer or seller should be aware that the illustrated multiples could be significantly different based on the facts and circumstances of the deal.

More specifically, the value of a home health business is driven by several factors, including:

1. Competition

2. Regulatory environment (i.e. Certificate of Need or ability to receive Medicare license)

3. Size as measured by revenue

4. Payor mix

5. Profitability

6. Top and bottom line growth potential

7. Ability for any third-party operator to improve operations

8. Reputation and quality of services

9. Affiliations or associations

10. Key post-transaction terms and conditions

Post-transaction contractual arrangements are almost always a part of a merger, acquisition or strategic partnership. Management agreements are commonly found in home health joint ventures. The fees set forth in these agreements should be considered as part of the decision making process. These arrangements impact the financial viability of the strategy and could pose compliance risks if not set at the right price, namely Fair Market Value (FMV)12. In addition to appeasing Stark and Anti-kickback regulations, the fair market value standard helps to protect tax-exempt organizations from private inurement issues.

Although there are numerous regulatory considerations involved in any healthcare arrangement, FMV tends to be one of the most highlighted by legal counsel, and time-consuming to tackle. Because the parties involved in most of these arrangements are in a position to refer patients to one another, the price of the transaction, or fee in any agreement, must be established at FMV, absent considering referrals. Said another way, when establishing a transaction price or agreement fee, the valuation methodology must be conducted in such a way that referrals are not part of the analysis. To the healthcare industry newcomer, this can come as quite a surprise and be counter-intuitive, but the regulatory risks are giant. To protect parties from this risk, it is common for both counsel and the valuation firm to be specialized in healthcare, with a keen understanding of the industry and regulatory guidance. Likewise, reimbursement changes and other regulatory risks which may impact the value of a deal require professionals focused purely on the healthcare industry, and ideally home health specifically.

Bottom Line

The outlook for home health transactions is strong as the segment is likely to be a significant piece of the solution to rising healthcare costs. The observed industry fragmentation and growing importance of home health as a preferred patient destination will continue to create robust joint venture and acquisition opportunities. As such, there is an increasing interest from health systems to evaluate their home health strategy. Any opportunity evaluation should consider the unique financial and regulatory nuances of the healthcare industry. So, will your health system be in or out?

1 Irving Levin Associates estimates for 2016.

2 Based on National Health Expenditure Accounts (NHEA) Home Health Care information and The Office of the Actuary at the Centers for Medicare and Medicaid Services (CMS), 2016-2025 projection. Covers medical care provided in the home by freestanding home health agencies (HHAs). These freestanding HHAs are establishments that fall into NAICS 6216-Home Health Care Services. This industry comprises establishments primarily engaged in providing skilled nursing services in the home, along with a range of the following: personal care services; homemaker and companion services; physical therapy; medical social services; medications; medical equipment and supplies; counseling; 24-hour home care; occupation and vocational therapy; dietary and nutritional services; speech therapy; audiology; and high-tech care, such as intravenous therapy.

3 Ibid.

4 Kindred’s acquisition of Gentiva in 2015 positioned the organization as the largest operator of home health services.

5 LexisNexis 2015 Home Health Agencies Ranking.

6 MedPac, A CMS audit in 2010 suggested agencies overstated expenses in their cost reports to Medicare. Since 2001, Medicare has been basing their fee-for-service reimbursement to home health agencies, in part, using a mark-up on cost assumption. Due to the results of the CMS audit, Medicare implemented an annual rebasing reduction to home health reimbursement. These rebasing adjustments have be partially offset by annual payment updates each year in 2014-2017. Additionally, CMS has increased their scrutiny on home health service fraud and abuse through various regulatory and compliance standards since the CMS audit.

7 October 31, 2016, AHA News Now, CMS releases home health final rule for CY 2017.

8 A set of standards which agencies must comply in order to get paid by Medicare.

9 35th Annual JP Morgan Healthcare Conference, January 2017, page 8 of presentation materials.

10 March 14th, 2017, Barclays Global Healthcare Conference – Benjamin Breier, Chief Executive Officer, Kindred Healthcare, Inc.

11 Source CapitalIQ & Public Filings as of 12/31/2016.

12 Stark law defines Fair Market Value as the value in an arm’s-length transaction, consistent with the general market value. “General market value” means the price that an asset would bring as the result of bona fide bargaining between well-informed buyers and sellers who are not otherwise in a position to generate business for the other party, or the compensation that would be included in a service agreement as the result of bona fide bargaining between well informed parties to the agreement who are not otherwise in a position to generate business for the other party, on the date of acquisition of the asset or at the time of the service agreement. Usually, the fair market price is the price at which bona fide sales have been consummated for assets of like type, quality, and quantity in a particular market at the time of acquisition, or the compensation that has been included in bona fide service agreements with comparable terms at the time of the agreement, where the price or compensation has not been determined in any manner that takes into account the volume or value of anticipated or actual referrals.

The views, opinions and positions expressed within these guest posts are those of the author alone and do not represent those of Becker’s Hospital Review/Becker’s Healthcare. The accuracy, completeness and validity of any statements made within this article are not guaranteed. We accept no liability for any errors, omissions or representations. The copyright of this content belongs to the author and any liability with regards to infringement of intellectual property rights remains with them.