This content is sponsored by Urgent Care Partners

Health systems that want relationships with these unattached individuals must be willing to meet them where they are along their healthcare journey. Regardless of the clinical enterprise’s desire to connect everyone with a long-term physician relationship, responsive health systems will recognize they cannot form relationships through experiences that leave individuals unsatisfied. These relationships are particularly important at the individual’s first point of contact with the healthcare system.

The first healthcare touch points have unique influence. Studies continue to show that once an individual interacts with a provider, the vast majority will follow that provider’s near-term clinical advice. In a competitive environment, whoever controls the first touch points will be able to best influence patients’ secondary decisions and thereby help guide patients into a particular health system.

Historically, the first touch points have been either a physician office or an emergency room. As health systems have sought to influence patients’ healthcare decisions, strong primary care physician enterprises are developing. However, the demands for convenience mean an ever-growing portion of first touch points are happening in other channels like urgent care.

Urgent care is a large (approximately 19 percent) and rapidly growing (6-10 percent per year) component of primary healthcare. Scheduled primary care is still growing, but only at a fraction of the rate of the urgent care channel. Because urgent care is growing at four times the rate of scheduled clinics, the share of the primary care visits over 10 years is expected to shift dramatically. The urgent care channel today is largely controlled by private physicians, investors and urgent care companies. Over the next several years, health systems will develop the urgent care platform as they did with their scheduled primary care investments.

The Urgent Care Market

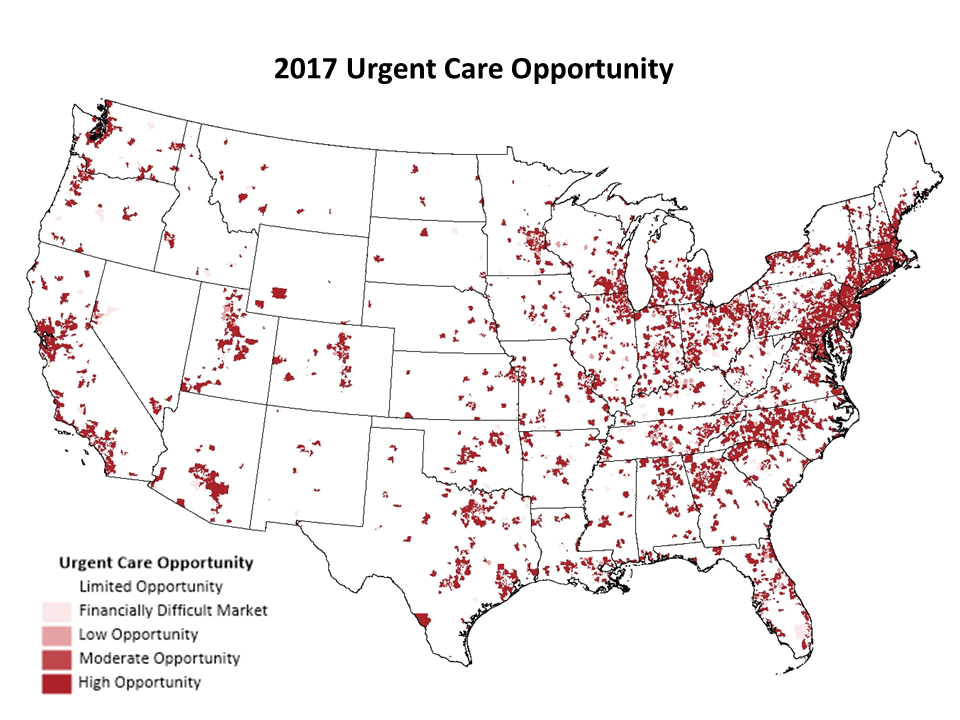

Many health systems ask if there are unmet needs in their communities. In the case of urgent care, the unmet need is typically access to convenient care. In early 2017, a strategy company, Health System Advisors, commissioned a study of the current national urgent care utilization and unmet demand. What they found was striking: With the recent rise of urgent care development, there is an estimated 22 percent unmet need for urgent care in markets where urgent care sites could be financially viable.

The unmet demand is so large that approximately 1,600 new urgent care sites can be supported generating nearly $3.5 billion in revenue.

For health systems seeking to grow, the urgent care channel presents a unique opportunity to grow their revenue, influence patients’ downstream choices and create a better experience for individuals desiring more convenience and better access.

Strategy + Implementation = Success

A health system urgent care strategy cannot succeed without successful implementation. Implementing a successful urgent care strategy has historically been difficult for health systems. Too often, the health system attempts to offer urgent care either as same-day schedule availability or by trying to replicate a low-acuity emergency room. Today’s modern urgent care models are more like a Starbucks than a physician’s office.

Here are five tips on how to begin.

1. Understand the consumer-perceived needs. To begin, start by evaluating your market to see if nontraditional providers are offering services patients traditionally receive from your system or if there are concierge or urgent care centers opening. If there are on-demand type providers arising, they are serving an unmet need or working to change the population’s expectations. In either case, your health system needs to begin developing an urgent care game plan.

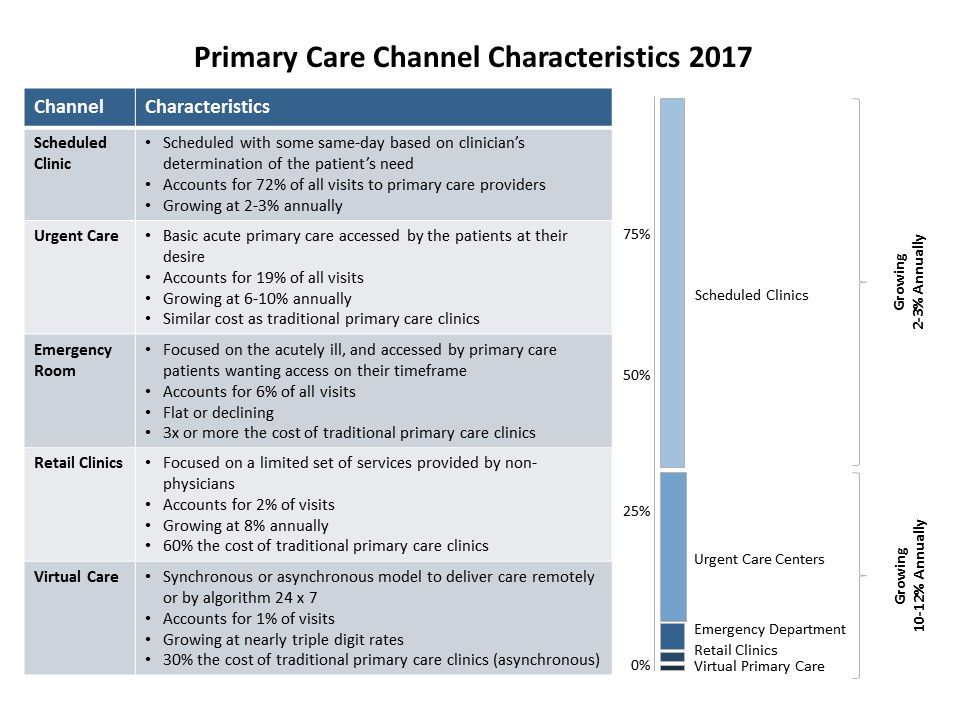

2. Evaluate your system’s primary care channels. Primary care today is delivered through five major channels.

Any urgent care planning process needs to understand where urgent care fits within the health system’s primary care delivery platform. Urgent care is experiencing much faster growth than traditional scheduled physician clinics. Between 2015 and 2020, urgent care is projected to grow 35 percent more than traditional scheduled primary care clinic volumes.

.PNG)

Evaluating your health system’s primary care channels process starts with a review of when and how patients can access your system. Gaining insight into how it feels to be an individual who wants to access care on their terms is key to redesigning urgent care channels. To do this, health system leaders should ask themselves the following questions: what someone would do if they wanted to see a primary care provider right now, how patients who don’t have a primary care provider in their system would get a physician appointment, what does it cost, how much paperwork needs to be filled out, etc. Factoring in this approach with a traditional primary care market plan will start providing both a market and channel viewpoint.

3. Build or engage the right capabilities to develop your urgent care division. Urgent care operations are fundamentally different from other parts of the health system. Urgent care is a highly consumer-focused, low-acuity service that demands the delivery model maintains the highest quality while rapidly serving the patients who arrive in a random pattern. As a result, health systems’ track record of providing financially accretive urgent care models is poor. On the other hand, private urgent care companies often make a 20 percent margin. The solution is not to give up urgent care to others, but internally build the right capabilities to participate in this growing trend.

.PNG)

Envisioning on-demand primary care delivered through a model with high levels of customer convenience and service is often closer to starting with a blank sheet than incrementally adjusting the current health system primary care models. To pull this off, health systems must give space and time to an urgent care development team that is not constrained by the existing processes and culture. At a minimum, this means hiring leaders who understand retail capabilities and often means bringing in development experts.

4. Design the urgent care model around the consumers’ demands not your historical approach. Urgent care is fundamentally a retail health service. To meet consumers’ demands for quality, service and convenience, a health system’s urgent care model must be more like Starbucks than the post office.

Starting with site selection in high-traffic retail settings, the urgent care division must rethink the provision of primary care from consumers’ point of view. Front-desk personnel should be thought of as clinical concierge rather than receptionists. Facility design should focus on rapid patient flow. Supplies and medications should focus on the top 30-40 requirements rather than all or none. Follow up and downstream coordination should be a core focus as the clinical diagnosis is completed.

.PNG)

Done correctly, the consumers will be highly satisfied and captured by the health system.

5. Move quickly. The market is rapidly moving. Who do you want to control this growing front door to your health system: you or a venture capital firm? Payers are also interested as a means to provide immediate primary care access without having to incur the expense of an ER visit. Moreover, the urgent care market is highly fragmented, offering market space for health systems (or nontraditional competitors) to capture and influence how urgent care develops.

Unless this is an organizational priority and your health system is moving rapidly, you are going to be outmaneuvered by competitors who are not constrained by your historical models of primary care.

The next wave of urgent care growth is just emerging. Health systems that want to influence the growing number of patients using this primary care channel must understand patient needs not being met today, know how new healthcare models are meeting those needs, create new retail-focused capabilities, and design integrated urgent care models around consumers’ demands. Those providers able to accomplish this feat will ride the growing wave and influence their population’s healthcare decisions at the first healthcare touch points.

Kate Lovrien is the Vice President of Strategy and Luke C. Peterson is the Vice President of Innovation at Urgent Care Partners. They can be contacted at Kate.Lovrien@UrgentCarePartners.com or Luke.Peterson@UrgentCarePartners.com. For more information contact UCP at 877.776.3639 or www.UrgentCarePartners.com.

More articles on patient flow:

Closed Missouri hospital plans to reopen as psychiatric facility after resolving issues with CMS

South Carolina hospital unveils pediatric ambulance

California behavioral health hospital burns down as wildfires spread

At the Becker's 11th Annual IT + Revenue Cycle Conference: The Future of AI & Digital Health, taking place September 14–17 in Chicago, healthcare executives and digital leaders from across the country will come together to explore how AI, interoperability, cybersecurity, and revenue cycle innovation are transforming care delivery, strengthening financial performance, and driving the next era of digital health. Apply for complimentary registration now.