This is a great time for hospital leadership and boards to reevaluate their strategies. This article contains eight core thoughts and concepts on strategic planning for hospitals.

1. Development of a strategy and strategic framework. There are several different frameworks that can be used to build a strategy. Hospitals need to assess their overall strategy. One concept as to strategic approach proclaims that an organization should make a clear choice as to (1) whether an organization wants to be a low cost leader, (2) whether it wants to be dominant in a specific niche or area, or (3) whether it wants to be a leader in being customer centric. Michael Porter, noted author of Competitive Strategy, uses a similar framework and groups strategies into three generic strategies (i.e., strategies that are applicable across industries): cost leadership, differentiation and focus. Porter argued that to be successful over the long term, a firm must select only one of these strategies. Otherwise, a firm will be “stuck in the middle” and will not achieve a competitive advantage.

He also states, “These generic strategies are not necessarily compatible with one another. If a firm attempts to achieve an advantage on all fronts, in this attempt it may achieve no advantage at all. For example, if a firm differentiates itself by supplying very high quality products, it risks undermining that quality if it seeks to become a cost leader. Even if the quality did not suffer, the firm would risk projecting a confusing image.”

Then, as a hospital starts to assess and implement its strategy, it must focus as much of the organization’s resources and energies as possible toward accomplishing these strategies and goals. In terms of evaluating which strategy to pursue, hospital leadership may often use a tool such as a traditional BCG matrix (pictured below) whereby a leadership team maps out areas into four quadrants: (1) their current strongest cash generating businesses (e.g., imaging, spine, orthopedics, oncology, etc.); (2) areas in which they have high growth opportunities and the potential to have a high market share; (3) areas in which they do not currently have high market share, but there is a possibility for high growth (possibly, e.g., an evolving area or a specialty program (i.e., attempting to understand where the future revenue opportunities are)); and (4) areas in which there is low market share and low growth, in essence, areas that BCG traditionally refers to as dogs

Boston Consulting Group Matrix

The hospital leadership should combine the mix of looking at the business lines through the BCG matrix, and also assess such questions as Porter would set forth. Do you, i.e., want to choose to be one of the three items outlined above: (1) a cost leader (traditionally in healthcare, this has not been the best position); (2) dominant in a specific niche (for example the hospital with the best orthopedics program and/or the best oncology program, or some other high value high growth area); or (3) do you simply want to be extremely customer centric. In assessing these questions, one may also assess (1) how achievable is the goal — how competitive is it — how well-situated is the system to achieve leadership in the area; and (2) if achievable, is it worth achieving? Is there sustainable profit and leadership? For example, if one of the cash cows of the business is a relationship with a specific payor or a specific physician group, a core part of the strategy might be to model the organization such that they can remain very, very close to that payor or that provider.

A hospital can also choose to be dominant in a few different niches and combine this with the concept of being outstanding to a certain group of customers. It can also help clarify its strategy by making sure it understands what it is not. Stanford Hospital Chief of Staff Brian Bohman, MD, for example, informed his team members that Stanford is "not a low cost hospital and [is] not likely to be a low cost leader in the near future." He said, "It's thus even more critical that we be a high quality and high satisfaction hospital.”

Many strategists state that you have to pick one clear area where you want to focus. We tend to believe that you can be both dominant in several niches and still very customer centric. It is very hard, however, to choose to be both dominant in several niches and/or truly customer centric, and at the same time a cost leader. In essence, the resources needed to be truly customer centric or to be dominant in a certain niche area typically don’t line up well with also being a complete cost leader in an area.

One can counter that if a very close payor relationship is a key goal, then being a cost leader may in fact be in sync with that type of customer centric notion. However, even with the concept of being a leader for a payor or dominant in such an area that you could drive down supply and equipment costs, we generally perceive that a goal would be to normalize costs but not to be a cost leader.

As a further note on choosing price leadership, please note the following. Differentiation based on price in healthcare traditionally has had limited success due to (1) the actual or perceived reluctance of patients to sacrifice any significant measure of quality for corresponding cost savings, (2) the lack of information available to compare cost and quality, and (3) the disconnect between the consumer of the service and the party who pays for the service. For example, where the consumer is insulated from the true cost of providing the service, as is the case with a great deal of health care services, the consumer has very little incentive to economize. A growing category of exceptions, however, revolves around insurance plans which differentiate in cost sharing and drive patients to be more inquisitive regarding costs and their share of costs.

2. Understand where your revenue is coming from. On a macro level, it is critical for a system to understand by service line — both by areas of care and often by referral source or generator of business — what are the key sources of revenues. [1] If a system has four service lines that comprise 85 percent of the business, a first goal of management is to align resources toward continuing to focus efforts on those four service lines. Often, this means deepening the strength in those areas and continuing to grow those areas. In a webinar on strategic planning for hospitals and ASCs, Bain & Company partner David Fleisch recommended that hospitals invest in their core service lines before expanding to new services. He said hospitals that expand new services without ensuring their core services are bound to face challenges in the future. At the same time, with the knowledge that the profitability of service lines changes over time, leadership also needs to have a keen eye on which areas are potential growth areas, then pick and determine a few of those areas to really concentrate a second set of resources on. Finally, there is a school of thought that essentially says a management team wants to spend zero or very little time on those areas that are true weaknesses and/or low growth and low revenue areas, and to not divert its time from its core cash flow generating activities and high growth potential areas. This kind of discipline can be hard to manage in practice where you see leadership focus on non-core outside efforts such as a market 70 miles away from a hospital’s home base or a specialty with very little revenue potential for the system, but that seemingly somebody cannot help themselves but be focused on. However, the results that come from such efforts are not nearly worth the cost and time that would have been better spent on the cash generating activities of the organization and the potential high growth areas for the organization. An example of abandoning a “dog” may include dropping a service area where your hospital has only one physician and loses money, or dropping entirely a low volume, low paying payor.

In assessing strategy, we are big believers in exploiting existing strengths of the practice first. For example, a system might first add existing depth and strength to its strongest areas. E.g., if the system’s profits come from oncology, orthopedics and imaging, it might spend a great deal of its time and dollars investing to strengthen and grow these areas. This may mean that available resources are used to fund new equipment, physician recruitment and marketing in these areas. Second, the hospital may diversify in possible high growth areas and where the system has had some success to date. At one hospital, they made the effort to develop leading service lines in neurosurgery and pain management, while the hospital reduced spending in other areas. Here, it became the regional leader in neurosurgical services. Its CEO told Becker’s Hospital Review that the hospital decided to be the one and only hospital in the area to really focus on this area. It added neurosurgeons, developed call coverage arrangements with other hospitals, invested in technology to support the neurosurgical practice and developed a substantial leadership position.

Here, a health system that is building on its strengths would also examine areas that are immediately adjacent to it strongest areas. This concept of building out from strengths to adjacent areas is articulated extensively by Bain & Company, Inc. in a well-noted book titled “Profit from the Core” by Chris Zook. Bain and Zook note that successful companies focus on: (1) reaching full potential in the core business, (2) expanding into a logical adjacent business surrounding that core, or (3) preemptively redefining the core business in response to market turbulence. Instead of focusing on taking advantage of the next "hot industry," Bain directors recommend that companies focus on strategy, competitive position, reinvestment rates and execution. They cite the example that the most successful sustained growth companies specialize in goods with lower growth, such as energy (Enron), beverages (Starbucks), and athletic gear (Nike).

In sum, a hospital must first decide, with thorough examination of its current businesses and opportunities, what it desires to excel in, and then dedicate a great majority of its resources to such efforts.

3. Normalize costs. In all areas, a system needs to make efforts to normalize costs. Even if a system does not intend to be the cost leader, it is critical that its employee costs, supply and equipment costs, and other types of costs, are in line with benchmarks. Often in healthcare there is a certain amount of economies of scale to achieve a required baseline cost curve for either employee/wage costs as a percentage of revenues or other costs as a percentage of revenue. In essence, in some situations, there is very little ability to amortize staffing costs, leadership costs, IT costs or other costs (if you want to have top quality leadership and top quality staff) unless you have a substantial enough operation to be able to spread those costs over a reasonably sized revenue base.

One tool that almost every hospital uses to control equipment, supply and other costs is the group purchasing organization (“GPO”) model. Some of the largest and most well-known GPOs are Premier, Inc., HealthTrust Purchasing Group, VHA and MedAssets. A recent study estimated that GPOs save the U.S. healthcare industry approximately $36 billion each year. [2]

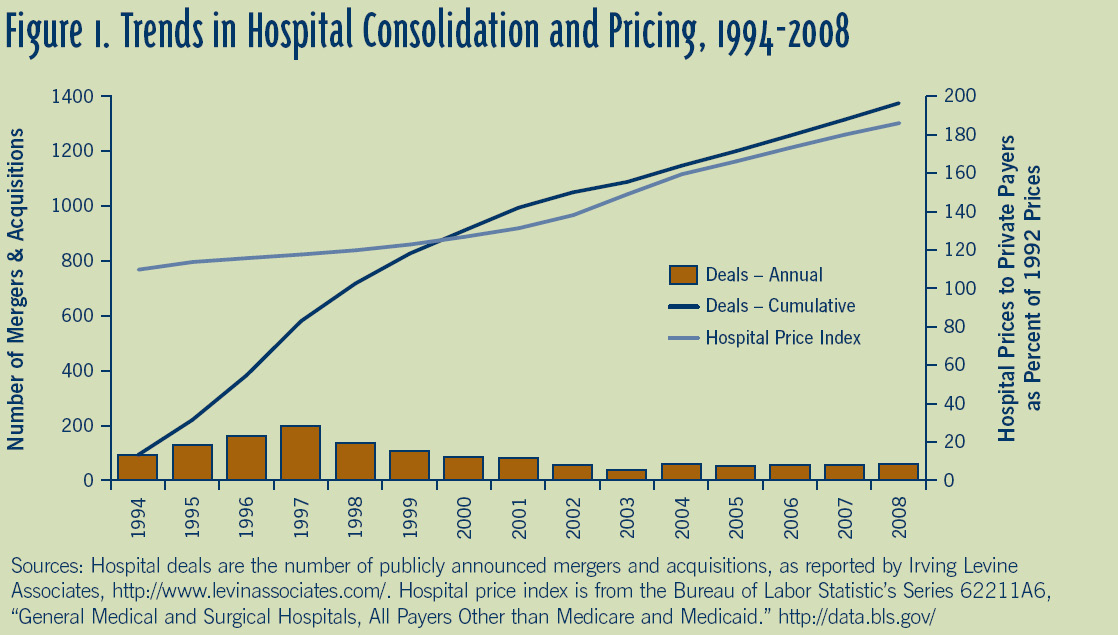

A recent increase in hospital consolidation activity highlights the need to minimize the cost structure supporting a hospital’s revenue stream. Hospitals are consolidating in order to achieve these economies of scale as a way to compensate for continual downward pressure on their reimbursement rates. Increases in internal efficiency and productivity can only counterbalance falling marginal revenue for so long before other means of cutting marginal cost are required. Although most studies have shown that economies of scale are achieved with increasing hospital size to 200 beds and beyond, some studies have also tied hospital consolidation to increased prices (see chart below). An alternative explanation for increases prices is an increase in quality, which can occur to due to an overall increase in patient volume or a focus on quality over costs differentiation, as noted above.

Source: William B. Vogt, PhD, Senior Economist, RAND Corporation, Hospital Market Consolidation: Trends and Consequences, EXPERT VOICES, National Institute for Health Care Management (November 2009).

4. Excel in billing, collections and managed care contracting. Many hospitals do not have leading managed care contracting capabilities internally. If your system is not large enough to maintain strength in this area internally, it may use outside consulting firms to obtain the best results on managed care contracting. Relative bargaining strength also tends to vary greatly with critical mass in a particular area. For example, in some areas of the country one payor dominates the market and smaller providers have very little ability to negotiate rates or terms. In addition to outside expertise, a larger scale can also help with these negotiations. For a large number of providers, Medicare reimbursement only covers a portion of the cost of providing services. Treating a Medicare patient is a money-losing proposition. As a result, commercial payor reimbursement rates become even more critical to financial success.

On billing and collections, most systems above a certain size will internalize billing and collections. Excellence in billing and collections is critical to financial success. In May, South Carolina's Greenville Hospital installed a new billing system to help close a $10 million budget gap and improve collections. In another example, by centralizing Catholic Health Initiatives' billing system, COO Michael Rowan helped save the organization $10 million in the last six months of FY 2009. Others have chosen to outsource billing and collections functions or to partner with a larger health system for administrative services and management.

5. Acquisitions and substantial investments. At this time, substantial acquisitions and investment must be measured very clearly against the core strategy of the organization. Does the investment help the system become dominant in an area that it desires to be dominant in, or does this acquisition or investment allow the system to be substantially more customer-centric? An example of a hospital that has implemented acquisitions successfully is Scott & White Memorial Hospital in Temple, Texas. Under the leadership of CEO Alfred Knight, M.D., Scott & White has aggressively expanded through mergers acquisitions, and investments. Mr. Knight said the key is to ensure that everyone is on the same page about the hospital’s best interests. "The lack of coordination in healthcare … creates redundancy and extra cost," he said in 2005. An acquisition in certain situations can also help bend the system’s cost curve. Moreover, in looking at this from a BCG matrix perspective, one would want to spend a great deal of their investment dollars in areas that they view as high growth areas where they can obtain a high market share.

There is also often a need to reinvest in high market share areas that are lower growth. In most situations, the first dollars invested in bigger acquisitions and investments should be spent very strictly in either protecting the cash cows of the organization or high growth, high possible market share areas. A secondary tranche of expense and resource allocation would go into promising question mark areas. On the flip side, unless there is some way to really focus resources on what is termed “a dog,” a low growth and low market share area, it generally makes sense to abandon efforts all together with respect to such area and sector.

Over the long term, in a changing reimbursement environment that is most likely to be a negative reimbursement environment, it is critical that the parties are cautious on their overall debt and leverage levels. This means very careful allocation of investment and acquisition dollars.

6. Stand alone systems. Unless a stand alone system has a clear reason for being — such as great dominance in an area and some level of substantial size — it may be very hard over the next 10 years to survive as a stand alone system. This is due to the need to allocate capital for reinvestment in systems and facilities, to physician integration, and potentially into new models of managed care and accountable care organizations. Many small stand alone systems do not have sufficient resources to allocate dollars to key objectives, because the investment required can be so substantial compared to the size of the system that it readily places the entire system at risk. In a Trustee magazine study of hospital long-term viability, Ryan Gish of Kaufman, Hall & Associates, Inc. stated that stand alone hospitals strain to remain strategically and financially competitive. According to the report, hospitals often enter into partnerships because they cannot offer state-of-the-art technology and attractive services on their own. According to AHA data, the United States has more than a thousand fewer hospitals today than it had in 1990, because of mergers, acquisitions, and closures – all of which are becoming increasingly commonplace.

7. Pension funding. Many larger systems with defined benefit plans have found themselves substantially underfunded over the last few years. The amount of money that needs to be funded for the unfunded benefit plans is really substantial and can create serious financial challenges to the stability of many institutions and their ability to refinance, and invest in new and important initiatives. Many systems will need to eliminate defined benefit plans and switch to other types of retirement plans as soon as possible. As a recent example, the high level of pension liabilities (along with overall debt load) was one of the primary factors in the decision of Caritas Christi Health Care to agree in principle to sell its operations to Cerberus Capital Management. Overall, the system has about $230 million in pension liabilities.

8. Physician integration. Most systems will have no choice but to use a mix of physician alignment strategies. These alignment strategies will include employing specialists and primary care physicians, joint venturing with specialists, and several types of arrangements that are in between these two models. This can include compensation relationships with physicians that are not employment relations or joint venture relations. Virginia Dempsey, president of Saint Joseph in London, Ky., told Becker's Hospital Review in May that alliances with physicians will be even more important under health reform. C. Duane Dauner, president of the California Hospital Association, agreed, saying that the lack of alignment between hospitals and physicians will cause major problems for hospitals who do not pursue a variety of strategies. We believe that most systems will need to have at least some significant number of employed physicians, if not as an offensive mechanism, as a defensive mechanism in a case where the market may quickly turn to an employed market model. They need to have the experience with employing physicians in case they need to have an infrastructure to do so. If they have to develop the infrastructure after a market has already moved toward the physician employed model, it can be very hard to catch up. One system we see made a substantial investment early on in an employed model, and now can bring in physicians by and large without having to create special deals for each group that joins the system. They have also developed a very distinct compensation fund and method of working with physicians such that they are now avoiding the concept of experimenting with every single group. The more experience a system has with this type of model earlier on and before it is needed, the better position the system is in to then adopt and work with such a model.

Another factor that will likely influence the move towards greater physician integration is the advent of formal accountable care organizations. In this model, the full spectrum of healthcare providers (primary care physicians, specialists and hospitals) partner with payors (Medicare and commercial payors) to manage overall cost and quality of care. Beginning in 2012, certain incentive payments will be available for those providers who are able to organize themselves into ACOs. A number of pilot programs and collaboratives are currently underway to start the process of integration.

1. Development of a strategy and strategic framework. There are several different frameworks that can be used to build a strategy. Hospitals need to assess their overall strategy. One concept as to strategic approach proclaims that an organization should make a clear choice as to (1) whether an organization wants to be a low cost leader, (2) whether it wants to be dominant in a specific niche or area, or (3) whether it wants to be a leader in being customer centric. Michael Porter, noted author of Competitive Strategy, uses a similar framework and groups strategies into three generic strategies (i.e., strategies that are applicable across industries): cost leadership, differentiation and focus. Porter argued that to be successful over the long term, a firm must select only one of these strategies. Otherwise, a firm will be “stuck in the middle” and will not achieve a competitive advantage.

He also states, “These generic strategies are not necessarily compatible with one another. If a firm attempts to achieve an advantage on all fronts, in this attempt it may achieve no advantage at all. For example, if a firm differentiates itself by supplying very high quality products, it risks undermining that quality if it seeks to become a cost leader. Even if the quality did not suffer, the firm would risk projecting a confusing image.”

Then, as a hospital starts to assess and implement its strategy, it must focus as much of the organization’s resources and energies as possible toward accomplishing these strategies and goals. In terms of evaluating which strategy to pursue, hospital leadership may often use a tool such as a traditional BCG matrix (pictured below) whereby a leadership team maps out areas into four quadrants: (1) their current strongest cash generating businesses (e.g., imaging, spine, orthopedics, oncology, etc.); (2) areas in which they have high growth opportunities and the potential to have a high market share; (3) areas in which they do not currently have high market share, but there is a possibility for high growth (possibly, e.g., an evolving area or a specialty program (i.e., attempting to understand where the future revenue opportunities are)); and (4) areas in which there is low market share and low growth, in essence, areas that BCG traditionally refers to as dogs

Boston Consulting Group Matrix

The hospital leadership should combine the mix of looking at the business lines through the BCG matrix, and also assess such questions as Porter would set forth. Do you, i.e., want to choose to be one of the three items outlined above: (1) a cost leader (traditionally in healthcare, this has not been the best position); (2) dominant in a specific niche (for example the hospital with the best orthopedics program and/or the best oncology program, or some other high value high growth area); or (3) do you simply want to be extremely customer centric. In assessing these questions, one may also assess (1) how achievable is the goal — how competitive is it — how well-situated is the system to achieve leadership in the area; and (2) if achievable, is it worth achieving? Is there sustainable profit and leadership? For example, if one of the cash cows of the business is a relationship with a specific payor or a specific physician group, a core part of the strategy might be to model the organization such that they can remain very, very close to that payor or that provider.

A hospital can also choose to be dominant in a few different niches and combine this with the concept of being outstanding to a certain group of customers. It can also help clarify its strategy by making sure it understands what it is not. Stanford Hospital Chief of Staff Brian Bohman, MD, for example, informed his team members that Stanford is "not a low cost hospital and [is] not likely to be a low cost leader in the near future." He said, "It's thus even more critical that we be a high quality and high satisfaction hospital.”

Many strategists state that you have to pick one clear area where you want to focus. We tend to believe that you can be both dominant in several niches and still very customer centric. It is very hard, however, to choose to be both dominant in several niches and/or truly customer centric, and at the same time a cost leader. In essence, the resources needed to be truly customer centric or to be dominant in a certain niche area typically don’t line up well with also being a complete cost leader in an area.

One can counter that if a very close payor relationship is a key goal, then being a cost leader may in fact be in sync with that type of customer centric notion. However, even with the concept of being a leader for a payor or dominant in such an area that you could drive down supply and equipment costs, we generally perceive that a goal would be to normalize costs but not to be a cost leader.

As a further note on choosing price leadership, please note the following. Differentiation based on price in healthcare traditionally has had limited success due to (1) the actual or perceived reluctance of patients to sacrifice any significant measure of quality for corresponding cost savings, (2) the lack of information available to compare cost and quality, and (3) the disconnect between the consumer of the service and the party who pays for the service. For example, where the consumer is insulated from the true cost of providing the service, as is the case with a great deal of health care services, the consumer has very little incentive to economize. A growing category of exceptions, however, revolves around insurance plans which differentiate in cost sharing and drive patients to be more inquisitive regarding costs and their share of costs.

2. Understand where your revenue is coming from. On a macro level, it is critical for a system to understand by service line — both by areas of care and often by referral source or generator of business — what are the key sources of revenues. [1] If a system has four service lines that comprise 85 percent of the business, a first goal of management is to align resources toward continuing to focus efforts on those four service lines. Often, this means deepening the strength in those areas and continuing to grow those areas. In a webinar on strategic planning for hospitals and ASCs, Bain & Company partner David Fleisch recommended that hospitals invest in their core service lines before expanding to new services. He said hospitals that expand new services without ensuring their core services are bound to face challenges in the future. At the same time, with the knowledge that the profitability of service lines changes over time, leadership also needs to have a keen eye on which areas are potential growth areas, then pick and determine a few of those areas to really concentrate a second set of resources on. Finally, there is a school of thought that essentially says a management team wants to spend zero or very little time on those areas that are true weaknesses and/or low growth and low revenue areas, and to not divert its time from its core cash flow generating activities and high growth potential areas. This kind of discipline can be hard to manage in practice where you see leadership focus on non-core outside efforts such as a market 70 miles away from a hospital’s home base or a specialty with very little revenue potential for the system, but that seemingly somebody cannot help themselves but be focused on. However, the results that come from such efforts are not nearly worth the cost and time that would have been better spent on the cash generating activities of the organization and the potential high growth areas for the organization. An example of abandoning a “dog” may include dropping a service area where your hospital has only one physician and loses money, or dropping entirely a low volume, low paying payor.

In assessing strategy, we are big believers in exploiting existing strengths of the practice first. For example, a system might first add existing depth and strength to its strongest areas. E.g., if the system’s profits come from oncology, orthopedics and imaging, it might spend a great deal of its time and dollars investing to strengthen and grow these areas. This may mean that available resources are used to fund new equipment, physician recruitment and marketing in these areas. Second, the hospital may diversify in possible high growth areas and where the system has had some success to date. At one hospital, they made the effort to develop leading service lines in neurosurgery and pain management, while the hospital reduced spending in other areas. Here, it became the regional leader in neurosurgical services. Its CEO told Becker’s Hospital Review that the hospital decided to be the one and only hospital in the area to really focus on this area. It added neurosurgeons, developed call coverage arrangements with other hospitals, invested in technology to support the neurosurgical practice and developed a substantial leadership position.

Here, a health system that is building on its strengths would also examine areas that are immediately adjacent to it strongest areas. This concept of building out from strengths to adjacent areas is articulated extensively by Bain & Company, Inc. in a well-noted book titled “Profit from the Core” by Chris Zook. Bain and Zook note that successful companies focus on: (1) reaching full potential in the core business, (2) expanding into a logical adjacent business surrounding that core, or (3) preemptively redefining the core business in response to market turbulence. Instead of focusing on taking advantage of the next "hot industry," Bain directors recommend that companies focus on strategy, competitive position, reinvestment rates and execution. They cite the example that the most successful sustained growth companies specialize in goods with lower growth, such as energy (Enron), beverages (Starbucks), and athletic gear (Nike).

In sum, a hospital must first decide, with thorough examination of its current businesses and opportunities, what it desires to excel in, and then dedicate a great majority of its resources to such efforts.

3. Normalize costs. In all areas, a system needs to make efforts to normalize costs. Even if a system does not intend to be the cost leader, it is critical that its employee costs, supply and equipment costs, and other types of costs, are in line with benchmarks. Often in healthcare there is a certain amount of economies of scale to achieve a required baseline cost curve for either employee/wage costs as a percentage of revenues or other costs as a percentage of revenue. In essence, in some situations, there is very little ability to amortize staffing costs, leadership costs, IT costs or other costs (if you want to have top quality leadership and top quality staff) unless you have a substantial enough operation to be able to spread those costs over a reasonably sized revenue base.

One tool that almost every hospital uses to control equipment, supply and other costs is the group purchasing organization (“GPO”) model. Some of the largest and most well-known GPOs are Premier, Inc., HealthTrust Purchasing Group, VHA and MedAssets. A recent study estimated that GPOs save the U.S. healthcare industry approximately $36 billion each year. [2]

A recent increase in hospital consolidation activity highlights the need to minimize the cost structure supporting a hospital’s revenue stream. Hospitals are consolidating in order to achieve these economies of scale as a way to compensate for continual downward pressure on their reimbursement rates. Increases in internal efficiency and productivity can only counterbalance falling marginal revenue for so long before other means of cutting marginal cost are required. Although most studies have shown that economies of scale are achieved with increasing hospital size to 200 beds and beyond, some studies have also tied hospital consolidation to increased prices (see chart below). An alternative explanation for increases prices is an increase in quality, which can occur to due to an overall increase in patient volume or a focus on quality over costs differentiation, as noted above.

Source: William B. Vogt, PhD, Senior Economist, RAND Corporation, Hospital Market Consolidation: Trends and Consequences, EXPERT VOICES, National Institute for Health Care Management (November 2009).

4. Excel in billing, collections and managed care contracting. Many hospitals do not have leading managed care contracting capabilities internally. If your system is not large enough to maintain strength in this area internally, it may use outside consulting firms to obtain the best results on managed care contracting. Relative bargaining strength also tends to vary greatly with critical mass in a particular area. For example, in some areas of the country one payor dominates the market and smaller providers have very little ability to negotiate rates or terms. In addition to outside expertise, a larger scale can also help with these negotiations. For a large number of providers, Medicare reimbursement only covers a portion of the cost of providing services. Treating a Medicare patient is a money-losing proposition. As a result, commercial payor reimbursement rates become even more critical to financial success.

On billing and collections, most systems above a certain size will internalize billing and collections. Excellence in billing and collections is critical to financial success. In May, South Carolina's Greenville Hospital installed a new billing system to help close a $10 million budget gap and improve collections. In another example, by centralizing Catholic Health Initiatives' billing system, COO Michael Rowan helped save the organization $10 million in the last six months of FY 2009. Others have chosen to outsource billing and collections functions or to partner with a larger health system for administrative services and management.

5. Acquisitions and substantial investments. At this time, substantial acquisitions and investment must be measured very clearly against the core strategy of the organization. Does the investment help the system become dominant in an area that it desires to be dominant in, or does this acquisition or investment allow the system to be substantially more customer-centric? An example of a hospital that has implemented acquisitions successfully is Scott & White Memorial Hospital in Temple, Texas. Under the leadership of CEO Alfred Knight, M.D., Scott & White has aggressively expanded through mergers acquisitions, and investments. Mr. Knight said the key is to ensure that everyone is on the same page about the hospital’s best interests. "The lack of coordination in healthcare … creates redundancy and extra cost," he said in 2005. An acquisition in certain situations can also help bend the system’s cost curve. Moreover, in looking at this from a BCG matrix perspective, one would want to spend a great deal of their investment dollars in areas that they view as high growth areas where they can obtain a high market share.

There is also often a need to reinvest in high market share areas that are lower growth. In most situations, the first dollars invested in bigger acquisitions and investments should be spent very strictly in either protecting the cash cows of the organization or high growth, high possible market share areas. A secondary tranche of expense and resource allocation would go into promising question mark areas. On the flip side, unless there is some way to really focus resources on what is termed “a dog,” a low growth and low market share area, it generally makes sense to abandon efforts all together with respect to such area and sector.

Over the long term, in a changing reimbursement environment that is most likely to be a negative reimbursement environment, it is critical that the parties are cautious on their overall debt and leverage levels. This means very careful allocation of investment and acquisition dollars.

6. Stand alone systems. Unless a stand alone system has a clear reason for being — such as great dominance in an area and some level of substantial size — it may be very hard over the next 10 years to survive as a stand alone system. This is due to the need to allocate capital for reinvestment in systems and facilities, to physician integration, and potentially into new models of managed care and accountable care organizations. Many small stand alone systems do not have sufficient resources to allocate dollars to key objectives, because the investment required can be so substantial compared to the size of the system that it readily places the entire system at risk. In a Trustee magazine study of hospital long-term viability, Ryan Gish of Kaufman, Hall & Associates, Inc. stated that stand alone hospitals strain to remain strategically and financially competitive. According to the report, hospitals often enter into partnerships because they cannot offer state-of-the-art technology and attractive services on their own. According to AHA data, the United States has more than a thousand fewer hospitals today than it had in 1990, because of mergers, acquisitions, and closures – all of which are becoming increasingly commonplace.

7. Pension funding. Many larger systems with defined benefit plans have found themselves substantially underfunded over the last few years. The amount of money that needs to be funded for the unfunded benefit plans is really substantial and can create serious financial challenges to the stability of many institutions and their ability to refinance, and invest in new and important initiatives. Many systems will need to eliminate defined benefit plans and switch to other types of retirement plans as soon as possible. As a recent example, the high level of pension liabilities (along with overall debt load) was one of the primary factors in the decision of Caritas Christi Health Care to agree in principle to sell its operations to Cerberus Capital Management. Overall, the system has about $230 million in pension liabilities.

8. Physician integration. Most systems will have no choice but to use a mix of physician alignment strategies. These alignment strategies will include employing specialists and primary care physicians, joint venturing with specialists, and several types of arrangements that are in between these two models. This can include compensation relationships with physicians that are not employment relations or joint venture relations. Virginia Dempsey, president of Saint Joseph in London, Ky., told Becker's Hospital Review in May that alliances with physicians will be even more important under health reform. C. Duane Dauner, president of the California Hospital Association, agreed, saying that the lack of alignment between hospitals and physicians will cause major problems for hospitals who do not pursue a variety of strategies. We believe that most systems will need to have at least some significant number of employed physicians, if not as an offensive mechanism, as a defensive mechanism in a case where the market may quickly turn to an employed market model. They need to have the experience with employing physicians in case they need to have an infrastructure to do so. If they have to develop the infrastructure after a market has already moved toward the physician employed model, it can be very hard to catch up. One system we see made a substantial investment early on in an employed model, and now can bring in physicians by and large without having to create special deals for each group that joins the system. They have also developed a very distinct compensation fund and method of working with physicians such that they are now avoiding the concept of experimenting with every single group. The more experience a system has with this type of model earlier on and before it is needed, the better position the system is in to then adopt and work with such a model.

Another factor that will likely influence the move towards greater physician integration is the advent of formal accountable care organizations. In this model, the full spectrum of healthcare providers (primary care physicians, specialists and hospitals) partner with payors (Medicare and commercial payors) to manage overall cost and quality of care. Beginning in 2012, certain incentive payments will be available for those providers who are able to organize themselves into ACOs. A number of pilot programs and collaboratives are currently underway to start the process of integration.

[1] A hospital should also examine which revenues are most at risk – by payor, by service line and otherwise.

[2] Eugene S. Schneller, Ph.D, The Value of Group Purchasing - 2009: Meeting the Need for Strategic Savings, April 2009.