Cost accounting in healthcare has never been more important, but is often considered too difficult, expensive or resource intensive for many healthcare organizations. Additionally, other critical applications such as EMRs have been the primary focus and resource drain over the last decade. However, our industry is undergoing significant change and pressure is coming from all stakeholders to lower the cost of healthcare. For those organizations without a cost accounting system, and there are many, perhaps up to 50 percent, it’s time to make it a priority.

Healthcare organizations need to correlate the cost of care with quality outcomes to effectively balance the delivery of quality patient care at a reasonable cost. Reimbursement is evolving towards value-based payment models that reward high quality and lower cost with shared savings. These payment models often include an element of risk, potentially substantial, in one form or another. Entering into a risk-sharing arrangement without understanding the details of your cost to deliver patient care exposes an organization to unnecessary financial risk.

Additionally, without a credible cost accounting system in place, hospitals are limited in their ability to identify cost drivers, implement and track cost reduction opportunities, utilize flexible and encounter-based budgeting, effectively negotiate payer contracts or successfully participate in ACOs. These are some of the many reasons cost accounting should be in every hospital, small to large, across the country.

Cost accounting defined

A cost accounting system is a system for recording, analyzing and allocating cost to the individual services provided to patients (e.g., medications, procedures, tests, room and board). Organizations without a cost accounting system rely on rudimentary methods such as the ratio-of-cost-to-charge. One RCC method utilizes Medicare’s cost report that is founded on a step-down cost allocation methodology. This methodology, designed for reimbursement, is not based on sound cost accounting principles and is not a substitute for a cost accounting system. The other RCC method is even less accurate, using total department cost as a percent of total patient revenue and applying that percentage across all department services.

Given current technology and limited patient specific cost data, the most credible and cost effective allocation method is a hybrid approach: advanced cost accounting. The charge and description master is utilized as the activity driver and relative value units as the “primary” basis for allocating costs. In addition, actual direct costs, time-based values, industry RVUs and non-chargeable activities are integrated where possible, providing the most comprehensive and credible approach.

Cost accounting is a team sport

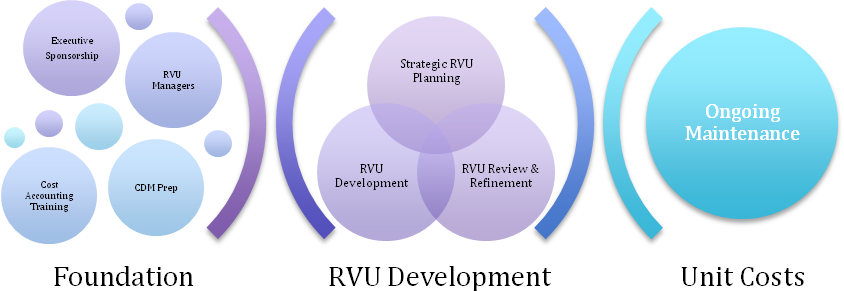

Implementing cost accounting is a “team sport” requiring expertise from across the organization. Clinical department managers or proxies play a key role in providing “technical estimates” of resource consumption levels when developing RVUs. The RVUs play the leading role as to where expenses are allocated and ultimately determine the accuracy of the individual CDM level unit costs. From my experience, this is the most critical and resource-intensive phase of the entire implementation process, and where there is a potential for less than desirable outcomes.

Cost Accounting Implementation Timeline

On the surface, RVU development seems straightforward enough. Clinical department managers or proxies estimate the amount of resources to perform each patient service using a numeric scale. Think of this scale as similar to the DRG weights. Accomplishing this task for most hospital organizations, with their typically vast and complex CDMs, often becomes a major resource and time black-hole. I suspect the RVU development effort is a primary reason as to why up to 50 percent of hospitals have not implemented a credible cost accounting solution and instead utilize inaccurate RCCs estimates or other inferior methods.

There are a number of factors that play into whether a RVU development effort is successful or not. Any one of these can derail an implementation and result in resource and time overruns and less than credible outcomes. After all, RVU development is more of an art than science. However, developing RVUs doesn’t have to be the roadblock to implementing a credible cost accounting system — a system that is quite as critical as any other required in today’s evolving, competitive and more transparent environment.

8 strategies to streamline your implementation

The challenges and resource intensity of RVU development can in fact be largely mitigated. From my years of experience and numerous cost accounting implementations, I recommend eight strategies to streamline the implementation effort while at the same time ensure unit cost quality and sustainability. These strategies at their core focus on cost vs. benefit, with the goal to strike a balance between the amounts of time clinical resources must spend developing and maintaining RVUs, vs. the desired quality of the unit cost data.

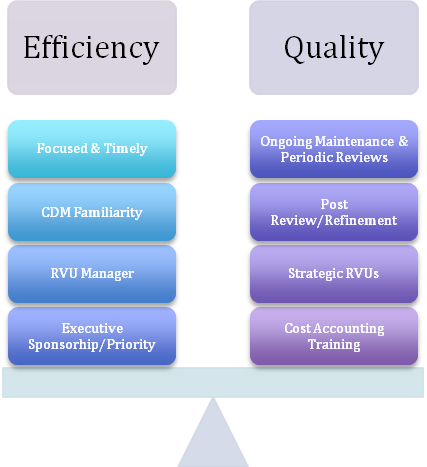

Strategy #1: Executive sponsorship

Cost accounting is typically viewed as a financial initiative and may not be a priority for clinical departments. In reality, cost accounting has broad organization-wide implications and most importantly benefits, and it cannot be implemented in a vacuum. Executive sponsorship and support across the senior management team are key to free resources and providing the initiative the focus it requires.

Most executive teams have strong interest in credible cost data and welcome any initiative that will help the organization make better-informed decisions. Making a comprehensive presentation to the senior management team is an effective way to ensure highest levels of the organization understand the investment of resources required and the value that an advanced cost accounting solution will provide the organization.

Strategy #2: RVU manager

Each clinical department will provide one or two resources involved in RVU development. I refer to this role as the “RVU manager,” and it is very important this person has thorough knowledge of departmental operations and is engaged throughout the RVU development process. There is a learning curve, and the development cycle tends to be iterative with RVU refinements made along the way. Continuity is key, and trading off the role between various staff will hinder implementation tasks and timing and jeopardize the end result.

The time commitment for the RVU manager role varies based on the following factors:

- Complexity and size of the department and its CDM

- How knowledgeable the individual is of department operations and resource consumption

- How familiar the individual is with the department’s individual CDM service codes

- Whether or not industry, actual cost, time-based values or CDM logic can be utilized over developing RVUs from scratch

Strategy #3: CDM familiarity

More and more patient charges are automated, and familiarity of the individual service codes should not be assumed. The typical CDM with its vast amount of service codes and sometimes-cryptic abbreviations can be problematic when developing RVUs. Department RVU managers must be familiar with the various service codes.

I am making a particular point of this because from my experience oftentimes the individual assigned to the RVU manager role has not been prepared in this regard. I suggest including CDM familiarity validation in the work plan and allow time to take corrective measures if necessary before moving forward. Sometimes what is necessary is to conduct a review session with the individual(s) that maintains the CDM and the department’s RVU manager to clarify service code descriptions/abbreviations.

Strategy #4: Cost accounting training

The RVU managers need a brief training course that covers cost accounting concepts, purpose and use both at the department and organization-wide level, basic cost accounting calculations, an introduction to the RVU development process, a description of the RVU manager role and the key benefits to the organization.

Covering these topics early in the process to ensure all participants are ready, able and willing to move forward and will provide the RVU managers with a solid foundation and context upon which to develop their RVUs. To build upon this base of knowledge, future training should include topics in flexible budgeting, price/mix/volume/efficiency variances and case-based/strategic budgeting.

Strategy #5: Strategic RVUs

Advanced cost accounting relies on RVUs primarily, but other data/techniques as previously discussed are utilized as well. The experienced implementer knows where to focus the RVU manager’s expertise and when and where to utilize other data and techniques such as actual cost, staffing ratios, industry RVUs, CDM logic and so on. Each department and cost category should be assessed individually. Also, focusing initially on high volume/revenue service codes and the highest expense categories help to minimize the initial RVU development effort. My philosophy is for subject matter experts to complete as much of the work as possible and utilize the RVU managers’ expertise on a more focused basis.

Strategy #6: Focused and timely

RVU development works best when it is a concentrated and tightly managed effort over a short period of time. Stringing out the process makes it more difficult for clinical participants and the implementation will lose momentum. Planning and organization are key considering there are often 50 to 200 clinical participants involved. RVU managers need to be timely as well and schedule the time required to develop their RVUs. The previous strategy, strategic RVUs, can have a positive impact on the actual amount of time required by the RVU managers. For example, RVU managers for nursing departments can typically complete the entire effort from training to development and review in around four hours. There are additional departments that will require more time, but the eight strategies I have outlined will significantly reduce the work effort for these as well.

Strategy #7: Post review and refinement

Once the initial RVUs are developed and the unit costs calculated, it is now time to review and validate the data and RVUs. The unit cost data should be combed through to identify abnormalities first. Obvious errors should be cleaned up and an inventory of outstanding issues needing the RVU managers’ expertise logged.

The next step is to review this first round of RVUs along with the RVU managers. This step is important because it provides the RVU managers an opportunity to better understand how the RVUs impact the unit cost calculations. Include in the review and discussion cost accounting department-level reports along with the CDM service code volumes and RVUs by cost category. This should be conducted on a one-to-one basis to allow for explanations and to make any necessary RVU adjustments.

The RVUs will improve over time as the RVU managers gain experience and understanding of how RVUs impact the cost allocations. Taking them from oftentimes unfamiliar cost accounting concepts, through the use and application of their RVU effort, will result in credible unit costs. The “technical estimate” approach is considered approximately 85 percent as accurate as engineered standards and at significantly lower investment in time and resources.

Strategy #8: Ongoing maintenance and periodic reviews

CDMs change and service codes are added routinely. Keeping up as new service codes are added is more efficient and maintains the accuracy of the monthly and YTD unit cost calculations. Alternatively, waiting until the end of the year can have a measurable impact on unit cost quality. A best practice is to include RVUs with each new service code request, which is easily accomplished with a little coordination between the functional areas involved.

Lastly, departments should be periodically scheduled for a comprehensive RVU review. Each department’s RVUs should be reviewed every one to two years. Performing a rotating quarterly review of a handful of departments is much more manageable than addressing all departments at once. Cycling through departments in this way assures continuity, and each pass improves the RVUs and correspondingly the unit costs. Each organization is different, but typically it can take a couple of RVU development cycles before everyone is comfortable with his or her RVUs.

8 Strategies for RVU Development

Conclusion

RVUs play a primary role in advanced hospital cost accounting methods and require involvement from across the organization. Even though the scope of the effort can appear significant, effectively executing the eight strategies previously outlined will dramatically reduce the time and resource investment required. Utilizing all 8 strategies will streamline implementation, lesson the impact on clinical departments, ensure unit cost credibility, and typically shorten the implementation from one year or more to under six months.

Healthcare organizations need cost data to make informed decisions. Cost “guesstimates,” based on RCCs or other inferior methods, are not viable. Without credible and detailed cost data, it is essentially impossible for healthcare organizations to strategically manage their operations and minimize the impact of declining reimbursement. It is time for the hospitals that have not made the investment in cost accounting to do so and become better prepared for our challenging and changing industry.

Steve Imus has 28 years experience in hospital finance, Big 4 healthcare consulting and as co-founder of Organizational Intelligence. He used his experience in hospital financial management and performance improvement to address the issues of legacy DSSs and to provide healthcare organizations with innovative tools for performance management.

At the Becker's 11th Annual IT + Revenue Cycle Conference: The Future of AI & Digital Health, taking place September 14–17 in Chicago, healthcare executives and digital leaders from across the country will come together to explore how AI, interoperability, cybersecurity, and revenue cycle innovation are transforming care delivery, strengthening financial performance, and driving the next era of digital health. Apply for complimentary registration now.