The article below is reprinted with permission from The Capital Issue, a quarterly newsletter published by Lancaster Pollard.

Negative arbitrage (Infitialis arbitari) has historically been a manageable nuisance to hospitals considering tax-exempt bonds for funding construction projects — comparable, perhaps, to the geese congregating around the hospital campus’ pond. In recent years, however, the negative arbitrage budget line item has swelled. As a result, negative arbitrage has devoured precious funds for improvements, and in some cases made projects infeasible. It’s as if those geese (at least the children enjoy them…) have transformed into pre-historic pterodactyls (hide the children!). For some hospitals, the cost of negative arbitrage has become a bad-monster-movie metaphor. Why has negative arbitrage become so costly, when will its effect dissipate, and what mitigation strategies currently exist?

What is negative arbitrage?

Arbitrage, with respect to tax-exempt debt, is the difference between the interest rate a borrower pays on its debt and the interest rate the borrower can achieve by investing yet-to-be-spent debt proceeds.

In the mid-2000s, tax-exempt borrowers had the potential to make a profit (or positive arbitrage) on unspent bond funds. Currently, however, hospital borrowers must pay out more to investors than they take in from investments. This extra capitalized interest is negative arbitrage.

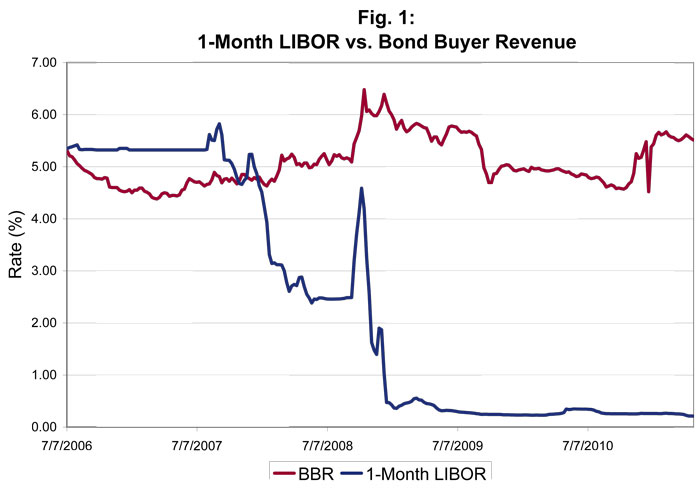

The U.S. Federal Reserve’s efforts to stimulate the economy, by taking short-term variable interest rates to near zero, has created a wide spread between the interest rate paid by a tax-exempt borrower (indicated in Figure 1 by the Bond Buyer Revenue Index, BBR) and that earned on investments (indicated by one-month Libor, a short-term interest rate benchmark). Hospitals may be borrowing at interest rates of 7 percent or higher, while bond proceeds invested during construction are earning almost nothing. As Figure 2 shows, the cost for a project can grow to financially unacceptable levels as interest rates and project size rise.

When will this large negative gap close? The economy must strengthen and then, hopefully, the Federal Reserve will be able to reduce its support and increase short-term interest rates. Based on historical precedent it will take several years for short-term taxable rates to reach the levels of tax-exempt fixed interest rates. Fortunately, there are several strategies for hospitals to consider.

Draw-down funding structures

One way to eliminate negative arbitrage is to ensure yet-to-be-spent project funds do not reside with a bond trustee. This can be accomplished by utilizing a draw-down funding structure. Similar to a home construction loan in functionality, borrowers pay interest only on funds that have been spent for project purposes. Two draw-down funding structures hospitals can utilize are private placements with commercial banks and FHA/HUD Section 242 insured taxable securities.

Private placements

Private placements let hospitals enter into loan agreements directly with commercial banks. The loan agreement may be with a single bank, or multiple banks via a syndicate arrangement. Commercial banks are familiar with draw-down bonds and generally offer more flexible structuring than trust indentures.

Private placements are often done as taxable transactions, but the interest rate may still be tax-exempt if the transaction is structured through a conduit issuer, and bond counsel provides the necessary tax-exempt opinion. Whether these additional expenses are justified is determined by cost/benefit analysis. A Lancaster Pollard client developing a $14.5 million addition in Kansas recently found that the tax-exempt private placement draw-down structure allowed them to avoid more than $1 million in negative arbitrage.

Federally insured taxable securities

Federally insured taxable securities work well for projects that are too big for commercial banks, or where a fixed interest rate is desired. The U.S. Department of Housing and Urban Development has been funding hospital projects through its Section 242 mortgage insurance program since 1968. The current loan portfolio includes health systems, sole community providers and critical access hospitals.

While the program can insure either tax-exempt bonds or taxable securities, only the taxable option allows for a draw-down structure. As a result, many HUD 242 borrowers, whether $20 million critical access hospitals or $200 million urban medical centers, are currently electing the taxable structure. Recent Lancaster Pollard clients avoided approximately $2 million and $3.3 million of negative arbitrage, respectively, on $25.9 million and $34 million projects.

Mitigating negative arbitrage

For a variety of reasons, a hospital may not be able to access an affordable financing option that permits a draw-down funding structure. In these cases, hospitals have several options to mitigate negative arbitrage:

1) Let the funds reside with the trustee in a money market fund. Under current conditions, however, money market funds produce almost no interest income.

2) Enter into a GIC, or Guaranteed Investment Certificate. This long-term savings option allows hospitals to receive a fixed interest rate payment and make withdrawals as needed. Rates, however, are fixed once they are set, and GICs offer far fewer options than they did prior to the market meltdown.

3) Hire an investment advisor to actively manage the funds.

Active management by an investment advisor means a hospital can build a customized investment strategy around the projected construction schedule. Funds that will be needed early in the process can be invested in short-term, highly liquid assets, while funds that will not be needed until farther along in the process can take advantage of longer-term investments and the potential for higher short-term interest rates as the economy improves.

As with the popularity of the horror movie genre, the headaches associated with negative arbitrage shall eventually pass. Unfortunately, unlike a summer movie season, the current negative arbitrage cycle may be around for several more years. In the meantime, be sure to work with an experienced investment bank capable of providing independent advice on all funding options.

Negative arbitrage (Infitialis arbitari) has historically been a manageable nuisance to hospitals considering tax-exempt bonds for funding construction projects — comparable, perhaps, to the geese congregating around the hospital campus’ pond. In recent years, however, the negative arbitrage budget line item has swelled. As a result, negative arbitrage has devoured precious funds for improvements, and in some cases made projects infeasible. It’s as if those geese (at least the children enjoy them…) have transformed into pre-historic pterodactyls (hide the children!). For some hospitals, the cost of negative arbitrage has become a bad-monster-movie metaphor. Why has negative arbitrage become so costly, when will its effect dissipate, and what mitigation strategies currently exist?

What is negative arbitrage?

Arbitrage, with respect to tax-exempt debt, is the difference between the interest rate a borrower pays on its debt and the interest rate the borrower can achieve by investing yet-to-be-spent debt proceeds.

In the mid-2000s, tax-exempt borrowers had the potential to make a profit (or positive arbitrage) on unspent bond funds. Currently, however, hospital borrowers must pay out more to investors than they take in from investments. This extra capitalized interest is negative arbitrage.

The U.S. Federal Reserve’s efforts to stimulate the economy, by taking short-term variable interest rates to near zero, has created a wide spread between the interest rate paid by a tax-exempt borrower (indicated in Figure 1 by the Bond Buyer Revenue Index, BBR) and that earned on investments (indicated by one-month Libor, a short-term interest rate benchmark). Hospitals may be borrowing at interest rates of 7 percent or higher, while bond proceeds invested during construction are earning almost nothing. As Figure 2 shows, the cost for a project can grow to financially unacceptable levels as interest rates and project size rise.

|

Figure 2 |

Rate 1 |

Rate 2 |

Rate 3 |

|

Hospital's interest rate |

5.00% |

6.00% |

7.00% |

|

Interest rate earned on unspend bond funds |

0.25% |

0.25% |

0.25% |

|

Difference |

4.75% |

5.75% |

6.75% |

|

Annual negative arbitrage per $1 million |

$47,500 |

$57,500 |

$67,500 |

When will this large negative gap close? The economy must strengthen and then, hopefully, the Federal Reserve will be able to reduce its support and increase short-term interest rates. Based on historical precedent it will take several years for short-term taxable rates to reach the levels of tax-exempt fixed interest rates. Fortunately, there are several strategies for hospitals to consider.

Draw-down funding structures

One way to eliminate negative arbitrage is to ensure yet-to-be-spent project funds do not reside with a bond trustee. This can be accomplished by utilizing a draw-down funding structure. Similar to a home construction loan in functionality, borrowers pay interest only on funds that have been spent for project purposes. Two draw-down funding structures hospitals can utilize are private placements with commercial banks and FHA/HUD Section 242 insured taxable securities.

Private placements

Private placements let hospitals enter into loan agreements directly with commercial banks. The loan agreement may be with a single bank, or multiple banks via a syndicate arrangement. Commercial banks are familiar with draw-down bonds and generally offer more flexible structuring than trust indentures.

Private placements are often done as taxable transactions, but the interest rate may still be tax-exempt if the transaction is structured through a conduit issuer, and bond counsel provides the necessary tax-exempt opinion. Whether these additional expenses are justified is determined by cost/benefit analysis. A Lancaster Pollard client developing a $14.5 million addition in Kansas recently found that the tax-exempt private placement draw-down structure allowed them to avoid more than $1 million in negative arbitrage.

Federally insured taxable securities

Federally insured taxable securities work well for projects that are too big for commercial banks, or where a fixed interest rate is desired. The U.S. Department of Housing and Urban Development has been funding hospital projects through its Section 242 mortgage insurance program since 1968. The current loan portfolio includes health systems, sole community providers and critical access hospitals.

While the program can insure either tax-exempt bonds or taxable securities, only the taxable option allows for a draw-down structure. As a result, many HUD 242 borrowers, whether $20 million critical access hospitals or $200 million urban medical centers, are currently electing the taxable structure. Recent Lancaster Pollard clients avoided approximately $2 million and $3.3 million of negative arbitrage, respectively, on $25.9 million and $34 million projects.

Mitigating negative arbitrage

For a variety of reasons, a hospital may not be able to access an affordable financing option that permits a draw-down funding structure. In these cases, hospitals have several options to mitigate negative arbitrage:

1) Let the funds reside with the trustee in a money market fund. Under current conditions, however, money market funds produce almost no interest income.

2) Enter into a GIC, or Guaranteed Investment Certificate. This long-term savings option allows hospitals to receive a fixed interest rate payment and make withdrawals as needed. Rates, however, are fixed once they are set, and GICs offer far fewer options than they did prior to the market meltdown.

3) Hire an investment advisor to actively manage the funds.

Active management by an investment advisor means a hospital can build a customized investment strategy around the projected construction schedule. Funds that will be needed early in the process can be invested in short-term, highly liquid assets, while funds that will not be needed until farther along in the process can take advantage of longer-term investments and the potential for higher short-term interest rates as the economy improves.

As with the popularity of the horror movie genre, the headaches associated with negative arbitrage shall eventually pass. Unfortunately, unlike a summer movie season, the current negative arbitrage cycle may be around for several more years. In the meantime, be sure to work with an experienced investment bank capable of providing independent advice on all funding options.