Your mission, should you choose to accept it, is to find capital to renovate or replace your aging hospital at an affordable cost. As a standalone hospital that doesn't rely on taxes, how hard can it be in 2012?

Let's find out. Median-ratios reports issued at the end of 2011 for non-profit hospitals and health systems by the "Big Three" credit rating agencies — Standard & Poor's, Fitch Ratings and Moody's Investor Service-indicate how industry and economic pressures are affecting the credit ratings of hospitals. These median ratios, by offering a snapshot of the finances of all rated hospitals in their individual portfolios, help in the comparison of credits across rating categories and are used to predict future sector performance.

What lies ahead?

Year-end median reports pointed to an overall improvement in performance for hospitals and health systems, but predicted challenging conditions for 2012. The Big Three warned of the growing pressures on the nonprofit healthcare sector with a still weak economy, selective credit markets, healthcare reform uncertainties, low patient volumes and the increasing number of uninsured/underinsured patients along with decreased reimbursement rates. These serious external threats continue to apply pressure on a hospital's bottom line while patients increasingly expect state-of-the-art facilities and services that provide quality and value.

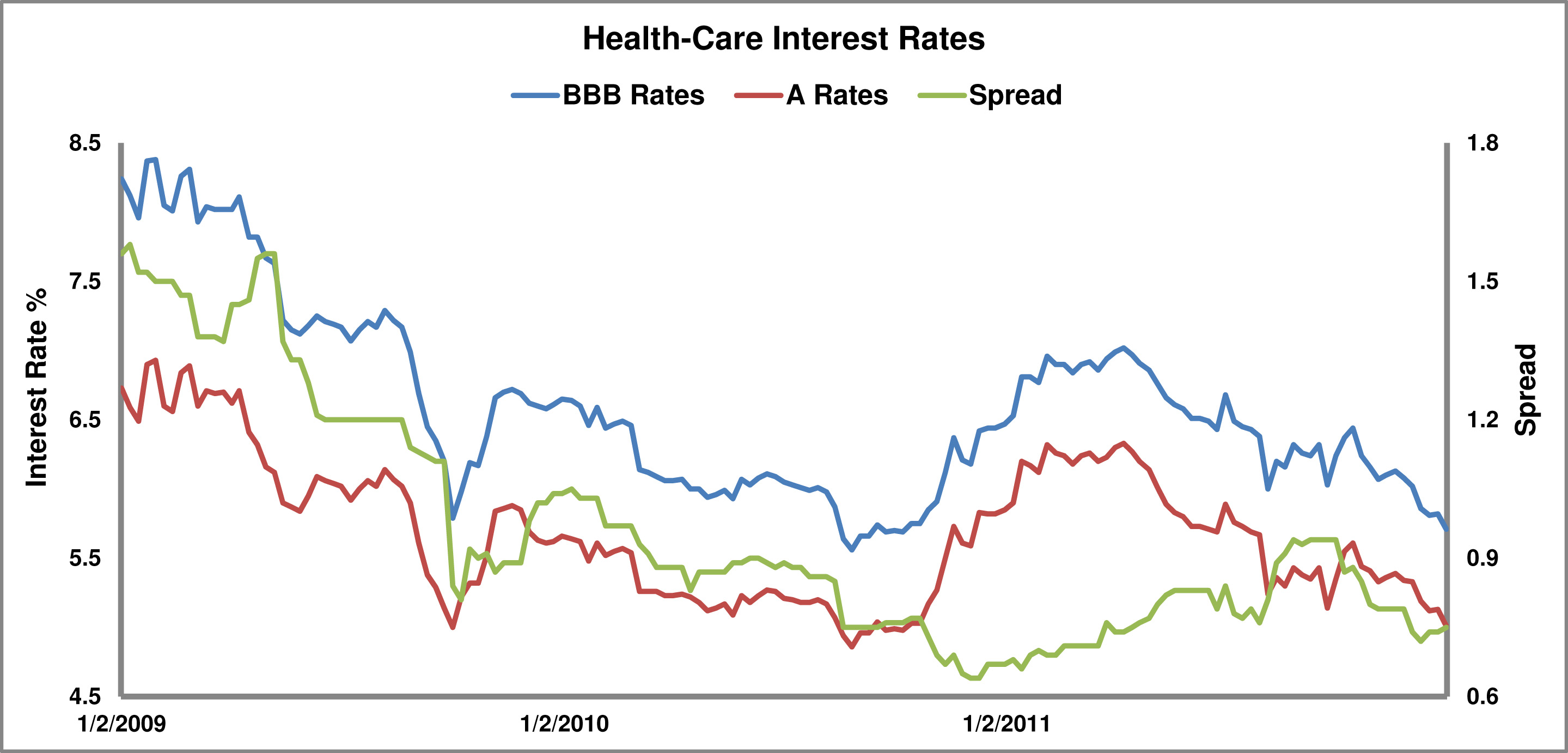

On the positive side, due to a waning supply of higher rated, investment-grade debt over the past three years, healthcare investors have moved down the credit spectrum in search of higher yields. Healthcare investors' increased risk tolerance is evident by the narrowing spread between BBB and A-rated 30-year bonds as investors search for higher returns. For example, the spread between Healthcare Baa/BBB and A/A 30-year offerings was 151 basis points in January 2009. However, as of January 2012, that spread has dropped by 53.6 percent to just 70 basis points. This has created an opportunity for lower rated, standalone hospitals to reduce their cost of capital to levels that more closely match their higher rated brethren. This landscape also requires a growing list of alternative capital-funding options, which low- to noninvestment-grade, standalone hospitals can use to revamp their aging plants or refinance existing higher cost debt.

Mission possible for BBB or below

Hospital leaders — particularly those of standalone, investment and noninvestment-grade facilities — need to be aware of what financing options are available to them in order to choose the best way to fund construction, renovations and new technologies and care-delivery methods. In addition to obtaining a debt rating, hospitals can consider the following routes to access long-term, fixed-rate capital:

Government-sponsored options

• The U.S. Department of Housing and Urban Development's FHA Sec. 242 Mortgage Insurance offers 100 percent nonrecourse debt at fixed-interest rates. The maximum term is 25 years after construction completion and loan-to-value is capped at 90 percent, which in some cases allows the loan to cover the entire actual project cost. Average operating margins must be positive and the average debt-service-coverage ratio must be equal to or greater than 1.25 for the previous three years.

• The U.S. Department of Agriculture offers two programs for rural hospitals – the Business & Industry Program (B&I) for communities of 50,000 or less and the Community and Facilities Program (CF) for communities of 20,000 or less. The B&I program offers a maximum term of 25 years and is best suited for projects of $10 million or less with the size of the loan guarantee varying between 60 percent and 80 percent depending on the loan size. The CF program provides direct and guaranteed loans (up to 90 percent) with a maximum term of 40 years. For both programs, the guarantee is generally issued upon construction completion.

• The New Markets Tax Credit Program through the U.S. Department of the Treasury may be used to finance capital projects for the health-care sector. NMTCP attracts investment capital to eligible low-income communities-rural or urban-by providing investors with a tax credit against their federal income tax return in exchange for making equity payments in Community Development Entities. The tax credit, which totals 39 percent of the original investment amount, is claimed over a period of seven years. The CDE will then make two loans to the borrower at below market rates, which require interest-only payments for the first seven years. Amortization on the loans begins after that initial period. The borrower pays no fees and most banks will treat investor-provided equity as project equity, reducing the amount of equity a non-profit borrower needs to contribute to finance the project. Additionally, many states offer state tax credits in conjunction with the federal program.

FHA Sec. 242 in action

Electra Memorial Hospital is a critical access hospital in northwest Texas. Challenged by a tight credit market and rural location Electra and its lender turned to the FHA Sec. 242 program to significantly renovate its 45-year-old facility and build a new wing of private rooms. As a result of the FHA mortgage insurance credit enhancement, Electra is expected to increase patient volume revenues through enhanced patient care and added services at AA-rated equivalent cost of capital.

Commercial options

All non-profit hospitals and governmentally-owned hospitals can issue revenue (or cash-flow supported) bonds, which are generally ratable depending on their underlying credit characteristics. Additionally, many governmentally-owned hospitals can issue general-obligation (or tax-supported) bonds, which also may be rated. These long-term, fixed-rate bonds are underwritten by a broker/dealer in a primary offering. Depending on market conditions and other available financing options, the hospital has the ability to use additional credit enhancement to further reduce its borrowing.

• A floating-rate index note may be a more preferable option than a fixed-rate bond. Basically, the index floater is a variable-rate bond with an initial index-floater mode or period (typically three to seven years) during which the bond pays an interest rate equal to a short-term index plus a fixed-credit spread. The bond can be a public offering or privately placed directly with a bank and is subject to renewal risk at the expiration of its initial term.

• Private placement, a common alternative today, is when tax-exempt bonds are privately placed with a bank or multiple banks or with a large bond fund. These bonds are negotiated with a select group of investors and disclosure requirements can sometimes be minimized and covenants made more flexible. If the private placements are deemed “bank qualified,” banks can deduct 80 percent of their costs and can pass along the savings to borrowers by means of a reduced interest rate. However, only $10 million in tax-exempt bonds can be designated as bank-qualified by a debt issuer in a year.

• The Federal Home Loan Bank letter-of-credit wrap gives a borrower the means to enhance taxable-debt issuances with a FHLB’s AA+ rating when an FHLB member bank provides the underlying LOC. This means smaller local banks could provide organizations access to investment-grade credit enhancement usually available only from larger banks. Nonprofits should still investigate FHLB LOCs because tax-exempt debt is not providing the cost break it has in the past. Also, taxable bonds require fewer upfront closing costs and fewer restrictions on the use of bond proceeds.

Private placement in action

Fulton County Health Center, a small hospital in northwest Ohio, has grown to include several specialty units, several medical clinics and a senior-living facility. FCHC, in good financial standing, faced an expiring LOC with a bank. A 5-year variable-rate direct purchase structure was selected. The new issue was a refunding of the earlier bonds plus cost of issuance. The transaction addressed the upcoming LOC expiration and removed the credit renewal risk during the 5-year term.

Despite mixed reviews from the Big Three for the healthcare sector in 2012, credit spreads have narrowed and options exist for standalone hospitals, such as Electra Memorial and Fulton County, to continue to finance their growth. A good understanding of all the options will help you obtain the required financing at reasonable terms to complete your mission.

Let's find out. Median-ratios reports issued at the end of 2011 for non-profit hospitals and health systems by the "Big Three" credit rating agencies — Standard & Poor's, Fitch Ratings and Moody's Investor Service-indicate how industry and economic pressures are affecting the credit ratings of hospitals. These median ratios, by offering a snapshot of the finances of all rated hospitals in their individual portfolios, help in the comparison of credits across rating categories and are used to predict future sector performance.

What lies ahead?

Year-end median reports pointed to an overall improvement in performance for hospitals and health systems, but predicted challenging conditions for 2012. The Big Three warned of the growing pressures on the nonprofit healthcare sector with a still weak economy, selective credit markets, healthcare reform uncertainties, low patient volumes and the increasing number of uninsured/underinsured patients along with decreased reimbursement rates. These serious external threats continue to apply pressure on a hospital's bottom line while patients increasingly expect state-of-the-art facilities and services that provide quality and value.

On the positive side, due to a waning supply of higher rated, investment-grade debt over the past three years, healthcare investors have moved down the credit spectrum in search of higher yields. Healthcare investors' increased risk tolerance is evident by the narrowing spread between BBB and A-rated 30-year bonds as investors search for higher returns. For example, the spread between Healthcare Baa/BBB and A/A 30-year offerings was 151 basis points in January 2009. However, as of January 2012, that spread has dropped by 53.6 percent to just 70 basis points. This has created an opportunity for lower rated, standalone hospitals to reduce their cost of capital to levels that more closely match their higher rated brethren. This landscape also requires a growing list of alternative capital-funding options, which low- to noninvestment-grade, standalone hospitals can use to revamp their aging plants or refinance existing higher cost debt.

Mission possible for BBB or below

Hospital leaders — particularly those of standalone, investment and noninvestment-grade facilities — need to be aware of what financing options are available to them in order to choose the best way to fund construction, renovations and new technologies and care-delivery methods. In addition to obtaining a debt rating, hospitals can consider the following routes to access long-term, fixed-rate capital:

Government-sponsored options

• The U.S. Department of Housing and Urban Development's FHA Sec. 242 Mortgage Insurance offers 100 percent nonrecourse debt at fixed-interest rates. The maximum term is 25 years after construction completion and loan-to-value is capped at 90 percent, which in some cases allows the loan to cover the entire actual project cost. Average operating margins must be positive and the average debt-service-coverage ratio must be equal to or greater than 1.25 for the previous three years.

• The U.S. Department of Agriculture offers two programs for rural hospitals – the Business & Industry Program (B&I) for communities of 50,000 or less and the Community and Facilities Program (CF) for communities of 20,000 or less. The B&I program offers a maximum term of 25 years and is best suited for projects of $10 million or less with the size of the loan guarantee varying between 60 percent and 80 percent depending on the loan size. The CF program provides direct and guaranteed loans (up to 90 percent) with a maximum term of 40 years. For both programs, the guarantee is generally issued upon construction completion.

• The New Markets Tax Credit Program through the U.S. Department of the Treasury may be used to finance capital projects for the health-care sector. NMTCP attracts investment capital to eligible low-income communities-rural or urban-by providing investors with a tax credit against their federal income tax return in exchange for making equity payments in Community Development Entities. The tax credit, which totals 39 percent of the original investment amount, is claimed over a period of seven years. The CDE will then make two loans to the borrower at below market rates, which require interest-only payments for the first seven years. Amortization on the loans begins after that initial period. The borrower pays no fees and most banks will treat investor-provided equity as project equity, reducing the amount of equity a non-profit borrower needs to contribute to finance the project. Additionally, many states offer state tax credits in conjunction with the federal program.

FHA Sec. 242 in action

Electra Memorial Hospital is a critical access hospital in northwest Texas. Challenged by a tight credit market and rural location Electra and its lender turned to the FHA Sec. 242 program to significantly renovate its 45-year-old facility and build a new wing of private rooms. As a result of the FHA mortgage insurance credit enhancement, Electra is expected to increase patient volume revenues through enhanced patient care and added services at AA-rated equivalent cost of capital.

Commercial options

All non-profit hospitals and governmentally-owned hospitals can issue revenue (or cash-flow supported) bonds, which are generally ratable depending on their underlying credit characteristics. Additionally, many governmentally-owned hospitals can issue general-obligation (or tax-supported) bonds, which also may be rated. These long-term, fixed-rate bonds are underwritten by a broker/dealer in a primary offering. Depending on market conditions and other available financing options, the hospital has the ability to use additional credit enhancement to further reduce its borrowing.

• A floating-rate index note may be a more preferable option than a fixed-rate bond. Basically, the index floater is a variable-rate bond with an initial index-floater mode or period (typically three to seven years) during which the bond pays an interest rate equal to a short-term index plus a fixed-credit spread. The bond can be a public offering or privately placed directly with a bank and is subject to renewal risk at the expiration of its initial term.

• Private placement, a common alternative today, is when tax-exempt bonds are privately placed with a bank or multiple banks or with a large bond fund. These bonds are negotiated with a select group of investors and disclosure requirements can sometimes be minimized and covenants made more flexible. If the private placements are deemed “bank qualified,” banks can deduct 80 percent of their costs and can pass along the savings to borrowers by means of a reduced interest rate. However, only $10 million in tax-exempt bonds can be designated as bank-qualified by a debt issuer in a year.

• The Federal Home Loan Bank letter-of-credit wrap gives a borrower the means to enhance taxable-debt issuances with a FHLB’s AA+ rating when an FHLB member bank provides the underlying LOC. This means smaller local banks could provide organizations access to investment-grade credit enhancement usually available only from larger banks. Nonprofits should still investigate FHLB LOCs because tax-exempt debt is not providing the cost break it has in the past. Also, taxable bonds require fewer upfront closing costs and fewer restrictions on the use of bond proceeds.

Private placement in action

Fulton County Health Center, a small hospital in northwest Ohio, has grown to include several specialty units, several medical clinics and a senior-living facility. FCHC, in good financial standing, faced an expiring LOC with a bank. A 5-year variable-rate direct purchase structure was selected. The new issue was a refunding of the earlier bonds plus cost of issuance. The transaction addressed the upcoming LOC expiration and removed the credit renewal risk during the 5-year term.

Despite mixed reviews from the Big Three for the healthcare sector in 2012, credit spreads have narrowed and options exist for standalone hospitals, such as Electra Memorial and Fulton County, to continue to finance their growth. A good understanding of all the options will help you obtain the required financing at reasonable terms to complete your mission.

More Articles on Hospital Finance:

Opportunity Knocking: Taking Advantage of Low Short-term Interest Rates

The Importance of a Strong Investment Policy Statement

Becoming a (Financially Stable) System